Non-Random Walk Theory: Difference between revisions

From Dickinson College Wiki

Jump to navigationJump to search

No edit summary |

|||

| Line 60: | Line 60: | ||

---- | ---- | ||

[[Random Walk]] | [[ | [[Random Walk]] | [[Speculative Bubbles]] | [[Fundamental Analysis]] | [[Technical Analysis]] | [[Efficient-Market Hypothesis]] | [[Non-Random Walk Theory]] | [[Market Efficiency vs. Behavioral Finance]] | ||

Revision as of 02:45, 1 May 2007

- Economists Andrew W. Lo and A. Craig MacKinlay criticized Malkiel's Random Walk theory in their book, A Non-Random Walk Down Wall Street

Criticisms

- Short Term Momentum, Including Underreaction to New Information

- Lo and MacKinley pointed to the presence of some "momentum" in short-run stock prices. Momentum is a series of repeated price changes in the same direction. Lo and MacKinley also addresses what they believed to be a common phenomena of underreaction to new information. This means that the stock is undervalued and that you can profit by accurately assessing the new information in its entirely.

- Malkiel's Response

- The statistical dependencies giving rise to momentum are extremely small and unlikely to provide the opportunity to achieve excess gains. Momentum strategies (buying stocks that show positive serial correlation) produced positive relative returns in the 1990s but negative relative returns during 2000. The most predictive patters seem to disappear as quickly as they are published.

- The statistical dependencies giving rise to momentum are extremely small and unlikely to provide the opportunity to achieve excess gains. Momentum strategies (buying stocks that show positive serial correlation) produced positive relative returns in the 1990s but negative relative returns during 2000. The most predictive patters seem to disappear as quickly as they are published.

- Malkiel's Response

- Long Run Return Reversals

- Fama and French found that up to 40% of variation in long holding periods can be predicted with a negative correlation with past returns. This supports the contrarian strategy.

- Malkiel's Response

- Return reversal may be accounted for by efficient function of markets based on the volatility of interest rates. Stock prices must rise and fall to be competitive with bond prices. If interest rates revert to the median over time, this generates return reversals. Malkiel used a thirteen year experiment and simulated a strategy of buying stocks over a thirteen year period during the 1980s and 1990s that performed particularly poorly in the past 3-5 years. These stocks had higher returns in the next 3-5 years after performing poorly in the previous years. After this period the strategy failed.

- Malkiel's Response

- Predictable Pattern Based on Valuation Parameters

- Valuation ratios such as the price-earnings multiple or the divident yield of the stock market as a whole have considerable predictive power.

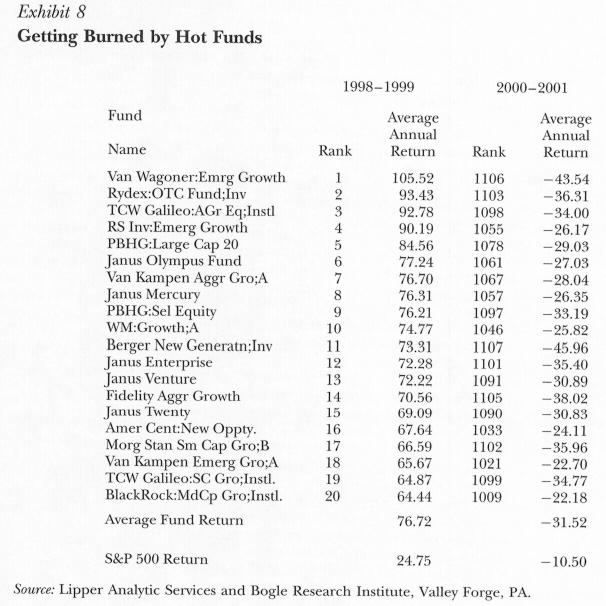

- 1. Initial Dividend Yields

- Dividend Yields are the ratio of a stock's dividend to its price

- Campbell and Shiller claim that initial dividend yields account for 40% of stock price variations

- Experiment:Divided the S&P 500 into deciles based on their initial dividend yields. They measured the dividend yield of the Standard & Poor 500 for each quarter starting in 1925. The experiment then mapped the 10 year returns for these stocks.

- Conclusion: Investors experience a higher returns on market baskets comprised of equities with high initial dividend yield.

- 2.Price - Earnings Multiples

- A similar experiment was done with price-earnings multiples of the S&P 500. As you can see from the graph (above) the deciles with higher price-earnings multiples generated lower returns relative to stocks of companies with lower price-earnings multiples. Again, Shiller claimed that study of the price-earnings multiples could account for 40% of all variations.

- 2.Price - Earnings Multiples

- Malkiel's Response

- Dividend Yields of stocks tend to be high when interest rates are high, and they tend to be low when interest rates are low. Therefore, the ability of initial yields to predict returns may simply reflect the adjustment of the stock market to general economic conditions. Moreover, D/P has been ineffective as a predictive mechanism since the mid-1980s. Although the dividend yield has been low for all ten year periods from the mid 1980s that ended in 2002, the returns have exceeded 15% on average. This contradicts the theory that stocks with a high initial dividend yield produce relatively higher returns.

- Even more important, this theory has never proven to be effective when predicting individual stocks. Also, there is no accounting for possible future alterations to corporations’ dividend behavior (which has become more seldom and decreased recently). Sample experiments, such as the “Dogs of the Dow” have failed to yield excess returns.

- With regards to the price to earnings ratio, since the 1987 the price-earnings multiples of the have risen from the low 20s to mid 20s in June 2002. During that time dividend to price ratios continued to fall around 3% or slightly lower. While this would spell lower returns according to Shiller’s work, returns from the index for the next ten years was 16.7%.

- Malkiel's Response

- The Size Effect

- One of the most accurate and consisten predictors of returns is the size effect. Smaller companies generally have higher relateve returns to their large company counterparts. Since 1926, small company stocks have had annual rates of return 1% greater than American large corporations. Fama and French's data segregated the stocks into deciles using their total capitalization. Decile contained the smallest 10% and so forth. The results, as displayed below, demostrated a clear tendency for portofolios of smaller stocks to generate larger relative returns.

- One of the most accurate and consisten predictors of returns is the size effect. Smaller companies generally have higher relateve returns to their large company counterparts. Since 1926, small company stocks have had annual rates of return 1% greater than American large corporations. Fama and French's data segregated the stocks into deciles using their total capitalization. Decile contained the smallest 10% and so forth. The results, as displayed below, demostrated a clear tendency for portofolios of smaller stocks to generate larger relative returns.

- Malkiel's Response

- There can be several explanations for this apparent flawless predictor. First, the data only includes the small companies that have survived. If you included to companies that were run out of business or filed bankruptcy the apparent higher returns would evaporate. In addition, since smaller firms then to be more risky (larger firms like Nike are not a threat to close shop any time soon), and the higher assumed risk can account for the large returns with the market remaining compatible with the Efficient Market Hypothesis. Here Malkiel discussed the proper measure of a stocks risk, its Beta value. The Beta value correlates the stock returns variance from the return of the entire market. With this in mind, the relationship between Beta and a stocks return was flat from 1963-1990. Simulated stock baskets from 1980-1990 have displayed no clear advantage of holding smaller stocks.

- Malkiel's Response

Historical Events Apparently In Contradiction With the Random Walk

- The Market Crash of Octobber 1987

- The Facts and the Challege

- In October of 1987 the market prices dropped by 33%. Behavorists cling to this example for the proof that psychological considerations must be responsible; thereby defying rational considerations. Critiques argue that such a rapid and significant drop, with no rapid change of hte basis elements of valuation during that time, signals market inefficiency. Malkiel highlights several factors with rational implicaitons investor's valuing of stock market prices:

- 1. Congress threatened to impose a merger tax

- 2. Secretary of the Treasury James Baker threatened to encourage a further fall in the dollar exchange value

- 3. Yields on long term treasury bonds rose 1.5% up to 10.5%

- In October of 1987 the market prices dropped by 33%. Behavorists cling to this example for the proof that psychological considerations must be responsible; thereby defying rational considerations. Critiques argue that such a rapid and significant drop, with no rapid change of hte basis elements of valuation during that time, signals market inefficiency. Malkiel highlights several factors with rational implicaitons investor's valuing of stock market prices:

- Implications of these Geopolitical Events

- The possibility of a merger tax would increase the cost of mergers. As a result, corporations would be dissaded from some potential mergers. The tax was large enough to end the merger boom by making such acqusitions prohibitively expensive. The further weakening of the dollar drove foreign investors away from holing American secruities, by increasing the potential risks. At the same time, this devaluing of our currency freighten domestic investors. Lastly, the increased yields on treasury bonds increased the appeal of the bond market. Since stocks and bonds are substitutive securities, invesotors began altering their holdings. Malkiel, through the use of some simply equations, demonstrates how small changes in "riskless" rate of interest on government bonds alone can cause large swings in the price of stock shares. The equation you use to explain this relationship is:

- r = D/P + g

- where r is the rate of return, D/P is the (expected) dividend yield, g is the long-term growth rate, and P is the appropriate price of the stock index ($/share).

- He assumes that r is the required rate of return for the market as a whole.

- The possibility of a merger tax would increase the cost of mergers. As a result, corporations would be dissaded from some potential mergers. The tax was large enough to end the merger boom by making such acqusitions prohibitively expensive. The further weakening of the dollar drove foreign investors away from holing American secruities, by increasing the potential risks. At the same time, this devaluing of our currency freighten domestic investors. Lastly, the increased yields on treasury bonds increased the appeal of the bond market. Since stocks and bonds are substitutive securities, invesotors began altering their holdings. Malkiel, through the use of some simply equations, demonstrates how small changes in "riskless" rate of interest on government bonds alone can cause large swings in the price of stock shares. The equation you use to explain this relationship is:

- The Market Crash of Octobber 1987

Random Walk | Speculative Bubbles | Fundamental Analysis | Technical Analysis | Efficient-Market Hypothesis | Non-Random Walk Theory | Market Efficiency vs. Behavioral Finance